E-commerce had a volatile 2023. From declining sales in luxury to behemoth partnerships to the resurgence of influencer marketing, the last 12 months experienced several changes and surprises that even the analysts were not expecting. Reflecting on the performance and strategies of social commerce platforms, brands and marketplaces in 2023 has set the scene for a fast-moving and competitive market for 2024. Omnia looks at how the previous year ended within e-commerce and what industry players and shoppers may expect in 2024, in addition to the innovation that might change the future of retail.

Social commerce will show its teeth

Within the e-commerce landscape, it was the expansion of social commerce that made the largest leaps and bounds, proving once again how it has become the largest growing sub-industry within retail and e-commerce with an expected value of $2 trillion in 2025.

Forbes predicted that social commerce is growing three times faster than e-commerce while the moves and counter-moves made in 2023 mirrored why: Meta and TikTok are not interested in your lunch selfies anymore. They’re interested in your likelihood to shop. With Meta’s new partnership with Amazon, allowing Facebook and Instagram users to shop Amazon ads directly in the app, a new era of e-commerce is forming that further increases Amazon’s control of the market and further drives Meta’s plans to create shopping-first platforms.

Other social commerce companies such as TikTok, which is owned by Tencent in China, will also be focusing on establishing itself as a legitimate e-commerce and influencer marketing platform in the West. TikTok Shop’s launch in the US in September is set to disrupt both the social commerce and marketplace arenas for 2024. TikTok and Instagram are each other’s biggest competitors, thickening the hunt for consumer attention and loyalty. Instagram and Facebook are still the world’s top choices over TikTok for buying products, however, the difference is incremental: In Germany, 46% of shoppers use Instagram while 42% use TikTok. In the US, it’s 42% and 40% respectively, and in the UK, TikTok surpasses Instagram as the platform of choice (39% vs 35%). Despite TikTok’s incredible growth and influence, Omnia predicts that Meta’s new Amazon deal will keep them out of the top position for the foreseeable future.

The Implications of TikTok's Ban on E-commerce Retailers

The potential ban of TikTok in the United States carries significant ramifications for e-commerce retailers, who have increasingly leveraged the platform for marketing, sales, and customer engagement. TikTok, known for its highly engaging short-form videos and robust algorithm, has become a powerful tool for brands seeking to reach a young, tech-savvy audience. Here’s an exploration of the key implications:

Loss of a Major Marketing Channel

- TikTok as a Marketing Powerhouse: With over 1 billion monthly active users worldwide, TikTok has emerged as a crucial marketing channel for e-commerce brands. The platform's unique algorithm promotes content virally, often reaching millions of users organically. For many retailers, TikTok has been instrumental in driving brand awareness and engagement through influencer partnerships, user-generated content, and creative campaigns.

- Impact of the Ban: If TikTok were to be banned, e-commerce retailers would lose access to this vast audience. Brands that have heavily invested in building a presence on TikTok would need to shift their strategies quickly. This disruption could lead to a temporary decline in visibility and engagement, impacting sales and customer acquisition efforts.

Shift to Alternative Platforms

- Exploring New Avenues: E-commerce retailers would likely diversify and redirect their marketing efforts to other social media platforms such as Instagram Reels, and YouTube Shorts. These platforms offer similar short-form video features, which can help brands maintain some continuity in their marketing strategies.

- Challenges and Opportunities: Transitioning to new platforms may require additional resources and time to build a comparable follower base and engagement level. However, this shift could also present an opportunity for brands to diversify their social media strategies and reduce dependency on a single platform.

Impacts on Sales and Revenue

- Sales Generation via TikTok: TikTok's "Shop Now" buttons and seamless integration with e-commerce platforms have enabled direct purchases within the app, boosting sales for many retailers.

- Revenue Risks: The ban would disrupt the revenue stream, especially for brands that have seen substantial sales through TikTok. Retailers would need to find alternative methods to drive direct sales, such as enhancing their websites' shopping experiences or investing in other social commerce tools.

Influence on Consumer Behaviour

- Consumer Habits: TikTok has influenced consumer behaviour by making shopping more interactive and engaging. The platform's algorithm personalises content based on user preferences, making it easier for brands to target potential customers effectively.

- Behavioural Shifts: Without TikTok, consumers might shift their attention to other platforms, altering the dynamics of online shopping. Brands will need to adapt their strategies to align with changing consumer behaviours and preferences.

Talk to one of our consultants about dynamic pricing.

AI and E-commerce in 2024

Artificial Intelligence (AI) is transforming e-commerce in various ways, and many technologies that retailers use daily are AI-driven, even if not immediately apparent. Here are six of the most common AI applications in e-commerce:

Personalised Product Recommendations:

Collecting and processing customer data about their online shopping habits is now easier than ever. Retailers rely on machine learning to capture data, analyse it, and use it to deliver personalised experiences, implement marketing campaigns, optimise pricing, and generate customer insights. Over time, machine learning will require less involvement from data scientists for everyday applications in e-commerce companies.

Retail analyst Natalie Berg shares: ‘’AI is going to make retailers smarter leaner more efficient. And it's going to make our experience as customers as you can tell. It's going to make it more personalized more relevant’’

Customer Segmentation

Access to more business and customer data, along with increased processing power, enables e-commerce operators to better understand their customers and identify new trends.

Smart Logistics

Machine learning's predictive powers shine in logistics, helping to forecast transit times, demand levels, and shipment delays. Smart logistics use real-time information from sensors, RFID tags, and similar technologies for inventory management and better demand forecasting. Over time, machine learning systems become smarter, building better predictions for supply chain and logistics functions.

Sales and Demand Forecasting

Especially in times after COVID-19, planning inventory based on real-time and historical data is crucial. AI can help with this. A recent McKinsey report suggests that investment in real-time customer analytics will continue to be important for monitoring and reacting to shifts in consumer demand, which can be harnessed for price optimisation or targeted marketing.

These applications highlight how AI is revolutionising e-commerce, providing enhanced personalisation, operational efficiency, and smarter business strategies.

Marketplaces will face stiffer competition with less market share

Niche marketplaces within luxury such as Yoox Net-A-Porter (YNAP), Farfetch and Matches almost ended in collapse in 2023, however, Farfetch was saved by South Korea’s e-commerce giant Coupang in a last-minute sale, Matches has been purchased by UK retailer Frasers for €60 million, while YNAP is still searching for a saviour to bring them into the black since the sale to Farfetch fell through.

According to Vogue Business, Amazon or Alibaba could potentially purchase YNAP, two of the world’s biggest e-commerce platforms, further strengthening their grasp on the marketplace landscape. As mentioned above, Amazon has continued its growth and consolidation by entering the social commerce space with Meta, which was announced in November, and the results of this deal will play out interestingly throughout 2024.

How will this affect other marketplaces? In 2024, marketplaces will feel the pinch of the Meta-Amazon coalition as an increasing number of lucrative vendors will turn toward Meta platforms to make sales and grow their brands. As a result, consumers will go where there is variety with a competitive price and an easier shopping experience. However, if more shoppers will be heading toward Meta platforms, marketplaces may be able to take advantage of the increased traffic with new advertising, sales and pricing strategies. Marketplaces other than Amazon will need to incentivise shoppers to choose their platform - whether it is via social media or not - to remain profitable.

Although Zalando ended off 2023 with declined quarterly sales, their new partnership with Highsnobiety has led Omnia to believe that they too have noticed the e-commerce success that lies within content. Europe’s largest marketplace has realised that many customers, especially Gen Z and millennial shoppers, buy into content and not products. The new platform, entitled Stories, creates fashion-related video content and provides news of collaborations and interviews with designers. “We know that customers are looking for inspiration and with Stories on Zalando we are doing exactly that: crafting highly engaging formats to show what’s new and what’s next in fashion,” says Zalando’s Senior Vice-President of Product Design Anne Pascual.

Brands will restrategise marketing and sales strategies to regain sales

Brands in multiple categories, especially in fashion, beauty and luxury, experienced a cooling period in 2023 that lasted longer than expected. For some, this will extend into 2024: Burberry’s shares have dropped 15% after they reduced their profit outlook thanks to a quieter-than-expected sales period over Christmas. Nike is cutting jobs and is set to reduce $2 billion in costs over the next three years amid dwindling sales. Gucci’s brand equity dropped 31% from 2022 to 2023, while L’Oréal and Lancome list 20% and 19% respectively.

Overall, the annual Kantar BrandZ report concluded that the world’s top 100 brands lost 20% of their value in 2023, leaving them on the back foot as 2024 gets underway which will see brands moving and shaking to get into a profitable, growthful place again.

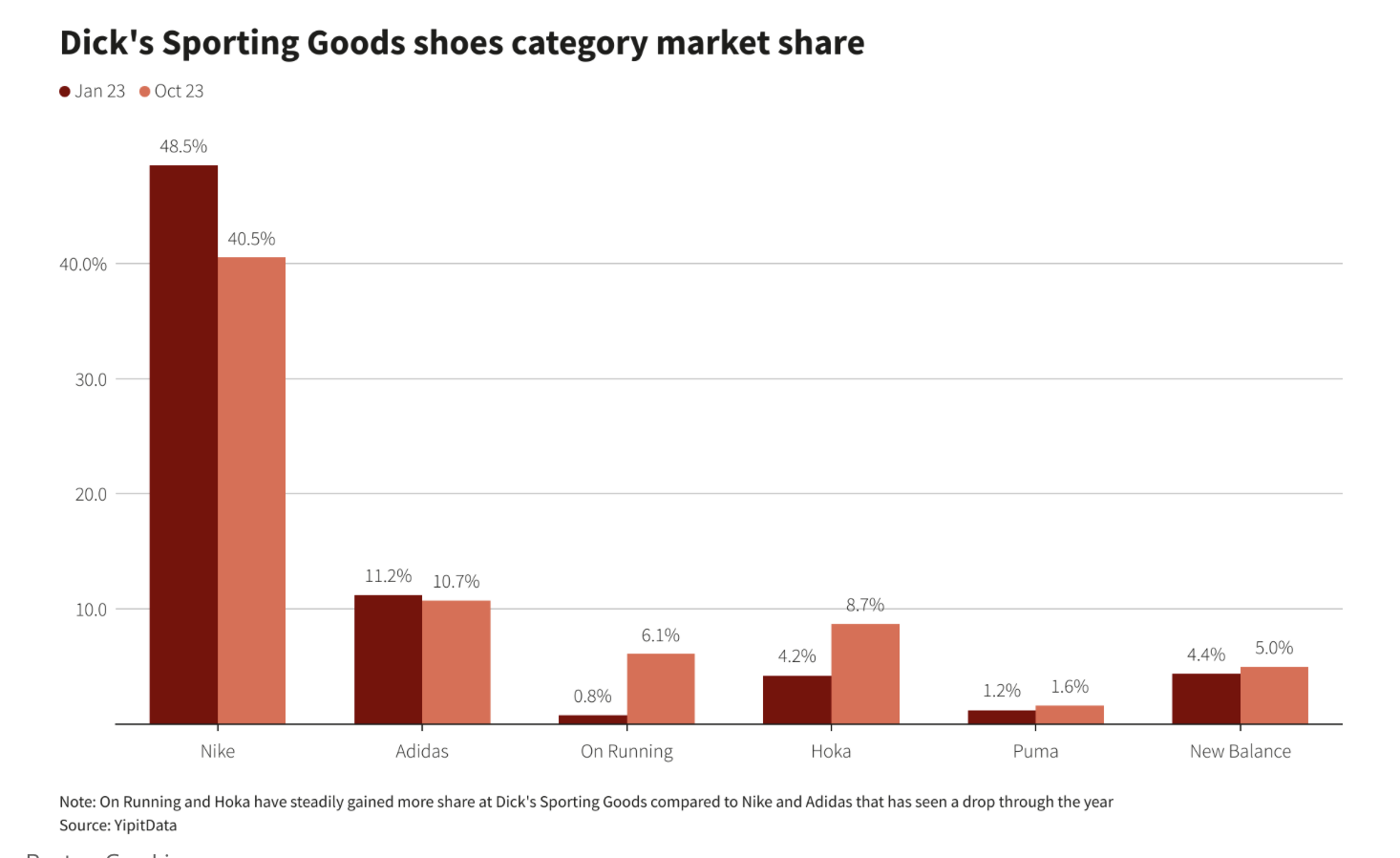

Despite the overall lookout, other brands in some verticals including sports apparel and performance footwear did well such as Swiss-owned running shoe maker On which saw third-quarter sales increase by 44% and HOKA, which consistently saw growth throughout 2023 and gained in market share.

In 2024, On is focusing on building its D2C channel which will cut into market share controlled by Adidas and Nike which have seen declining market share at Dick’s Sporting Goods, one of the US’s largest shoe retailers, while On and HOKA increase.

2024 trends in sports apparel include a transition from logo-heavy designs, which we saw gain prevalence within “quiet luxury”, to “quiet outdoors”. Brands like North Face and Arc'teryx will be focusing on gaining the attention of luxury buyers who want in on sportswear with a high-end feel.

Conclusion

As we move into the second half of 2024, the e-commerce landscape is set to become even more dynamic and competitive. The developments in 2023, including the rapid expansion of social commerce, strategic partnerships, and the resurgence of influencer marketing, have laid a robust foundation for the coming months.

Social commerce, driven by giants like Meta and TikTok, will continue to evolve, with new features and integrations aimed at enhancing the shopping experience. Meta's partnership with Amazon and TikTok's efforts to solidify its position as a key e-commerce player will significantly shape consumer behaviour and market dynamics. However, the potential ban of TikTok in the US could disrupt these trends, forcing brands to adapt quickly.

Marketplaces will face increased competition as the Meta-Amazon coalition draws more vendors and consumers to their platforms. This shift will compel other marketplaces to innovate and offer unique incentives to retain their market share. Strategic partnerships, such as Zalando's collaboration with Highsnobiety, highlight the importance of content-driven commerce in attracting and engaging younger audiences.

Brands, particularly those in fashion, beauty, and luxury, will need to re-strategise their marketing and sales approaches to recover from the prolonged cooling period of 2023. While some brands face continued challenges, others in niches like sports apparel are poised for growth, leveraging direct-to-consumer channels and tapping into emerging trends like "quiet outdoors."

In summary, e-commerce in the second half of 2024 will be characterised by rapid adaptation, and a focus on personalised, content-rich consumer experiences. Brands will need to leverage strategic partnerships with influential platforms and content creators to stay relevant. The successful players will be those who can seamlessly integrate innovative technologies and data-driven insights to create engaging, tailored shopping journeys for their customers.